TRAIN’d to win: Vehicles with tax reduction/exemption under TRAIN Law

Pickups like this Chevrolet Colorado enjoy exemption from excise tax

Last week I discussed the effect of the TRAIN (Tax Reform for Acceleration and Inclusion) Law on automobile prices. In a gist, the TRAIN Law’s new Ad Valorem Tax rates increased the price of some automobiles (specifically low-end to average-priced, and some high-end automobiles depending on the price range) and decreased the price of some automobiles (high-end automobiles based on a price range).

While the effect of the TRAIN Law on automobile prices vary, there is a clear advantage given by the TRAIN Law to certain types of vehicles.

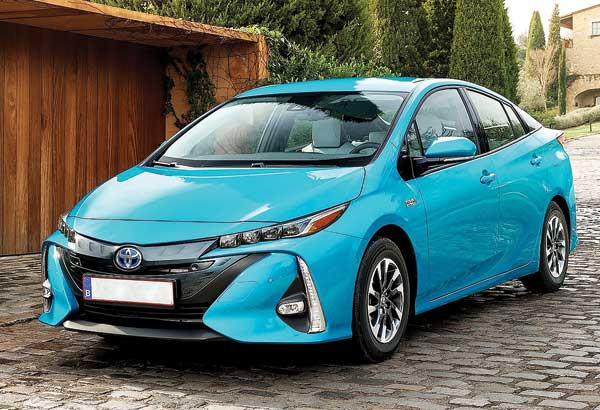

Compared to regular automobiles, “Hybrid Vehicles” are subject to only 50 percent of the excise tax rates imposed by the TRAIN Law. For instance, hybrid vehicles that cost over P1 million to P4 million are subject to a tax rate of 10 percent (compared to the 20 percent tax rate for regular vehicles of the same price). Hybrid electric vehicles refer to motor vehicles powered by electric energy (with or without provision for off-vehicle charging) in combination with gasoline, diesel or any other motive power. To be considered a hybrid electric vehicle, it must be able to propel itself from a stationary condition using solely electric motor. Some hybrid vehicles currently available in the Philippines include the Toyota Prius and the Lexus CT 200.

Bigger winners under the TRAIN Law are purely electric vehicles and pickup trucks, which are now EXEMPT from tax on automobiles. A “truck/cargo van” is defined as a “a motor vehicle of any configuration that is exclusively designed for the carriage of goods and with any number of wheels and axles.” However, the law explicitly states that pickups “shall be considered as trucks.” Thus, it appears that pickup trucks, which are for personal use or are not designed exclusively for carriage of goods, are still exempt from excise tax.

Toyota Prius

Also exempt from excise tax are automobiles used exclusively within Freeport zones. Thus, cars (regardless of the brand or model) used exclusively within Subic Freeport Zone or Clark Freeport Zone are exempt from excise tax under the TRAIN Law.

Generally, the TRAIN Law increased the excise tax rates on automobiles to generate revenue for the government’s infrastructure, health, education, employment, and social programs. However, it must be clarified that the TRAIN Law’s new tax rates don’t apply to ALL types of automobiles, at least not to the ordinary definition of automobiles. For purposes of applying the excise tax, the TRAIN Law defines “Automobiles” as any four- or more-wheeled motor vehicle regardless of seating capacity, which is propelled by gasoline, diesel, electricity or any other motive power. Notably, certain types of motor vehicles are NOT considered “automobiles” under the TRAIN Law such as buses, trucks, cargo vans, jeepneys/jeepney substitutes, single cab chassis, and special-purpose vehicles. Special purpose vehicles are motor vehicles designed for specific applications such as cement mixer, fire truck, boom truck, ambulance and/or medical unit, and off-road vehicles for heavy industries (not for recreational activities).

The effects of the TRAIN Law on automobile prices vary depending on the type of vehicles. While consumers cannot change the tax rates under the TRAIN Law, they can adjust their preferences (switch to hybrid or electric vehicles, or pickup trucks) to take advantage of the decreased tax rates or exemptions.

- Latest