Banks raise fees as TRAIN rolls out

MANILA, Philippines — Banks have started raising fees on certain transactions and services following the implementation of the first package of the Comprehensive Tax Reform Program at the start of the year.

Republic Act 10963, otherwise known as the Tax Reform for Acceleration and Inclusion Act (TRAIN) Law signed by President Duterte last Dec. 19 took effect last Jan. 1.

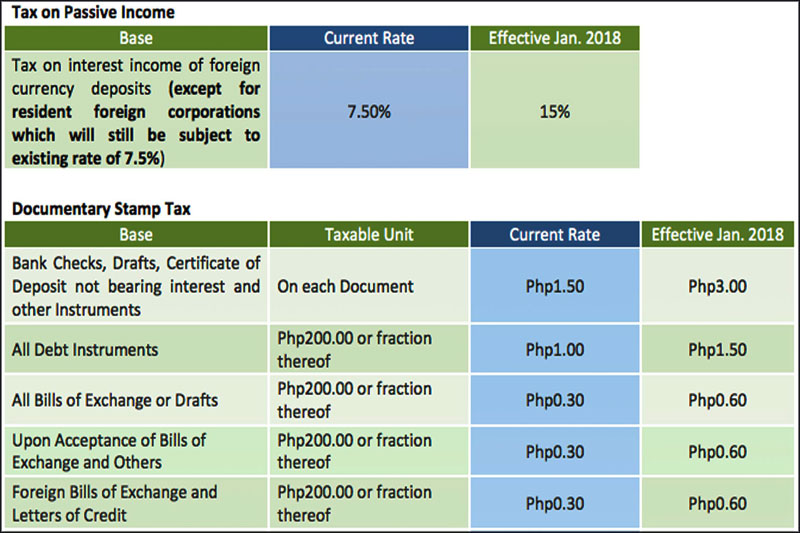

The law doubled the documentary stamp tax (DST) on bank checks, drafts, certificate of deposits not bearing interest; bills of exchange and letters of credit; mortgages, pledges, and deeds of trust; and certificates.

It also raised the DST on all debt instruments by 50 percent.

Furthermore, the TRAIN also doubled the tax on interest income in foreign currency deposit unit (FCDU) deposits to 15 percent from 7.5 percent.

BDO Unibank of retail and banking magnate Henry Sy has informed its clients about the new tax rates as well as the new cost of checkbooks as a result of the implementation of the new tax law.

Under the new rates, BDO said the DST on debt instruments such as peso time deposit would now be P1.50 per P200, while outward or inward foreign telegraphic transfer as well as outward foreign currency check would now cost P0.60 per P200.

The country’s largest bank said the DST on checkbook is now P3 per check and a personal checkbook would now cost P250, while a commercial checkbook would now cost P500.

“Please be advised that effective Jan. 1, there will be an increase in rates on DST on certain bank transactions and final withholding tax on interest on FCDU deposits in compliance with RA 10963,” Metropolitan Bank & Trust Co. of taipan George SK Ty said in a notice to clients.

Bangko Sentral ng Pilipinas Deputy Governor Chuchi Fonacier said authorities are now assessing the impact of the new TRAIN law on the banking industry.

“We’re still looking into its impact,” she said in a text message.

Raul Martin Pedro, executive vice president and treasurer at Security Bank Corp., said the reserve requirement ratio (RRR) imposed on banks must be lowered as the increase in DST would result to higher intermediation costs.

“Now that the tax reform law is being implemented, the RRR must be lowered to compensate for the higher intermediation costs which will possibly affect the expected returns of depositors,” Pedro said.

The RRR is the percentage of bank deposits and deposit substitute liabilities that banks maintain or deposit with the central bank. The Philippines has the highest ratio in the region currently pegged at 20 percent.

Adjusting policy settings such as the RRR of banks also reduces the intermediation costs while also controlling liquidity. For every one percent reduction, about P100 billion would be released into the financial system.

Pedro said that lowering the RRR could assist the banks in responding to the additional taxes.

“The passage of TRAIN will yield a domino effect in our national economy. By injecting adequate liquidity in our financial market, banks can help provide more opportunities for businesses to grow and keep the economy robust,” he added.

For his part, Metrobank senior executive vice president Ferdinand Antonio Tansingco said lower income taxes under the TRAIN would yield additional spending activity.

He pointed out there would be an increase in the demand for loans as businesses take this opportunity to expand their services in response to the projected higher purchasing power of consumers.

“Business expansion requires additional resources or infrastructure which they can avail of through banks,” he added.

Tansingco said banks are expected to have adequate financial resources to respond to such demand, but a high RRR may prevent banks from providing a steady supply of credit.

- Latest